Small business owners are always looking to save money on their tax bill, and marketing agency owners are no exception. One of the most common questions marketing agency clients ask, and that are often posed online is: “Can marketers take advantage of the QBI deduction?” The specifics of the QBI portion of the new tax law are complicated, for sure, and they require expert guidance to navigate. This post is meant to be a high-level overview of QBI, what it is, and how to take advantage of it if you’re a marketer.

What does QBI stand for?

QBI stands for Qualified Business Income.

What is the QBI deduction?

The QBI deduction is a tax deduction which came into being when the president signed the Tax Cuts and Jobs Act (TCJA) into law in December of 2017. The QBI deduction is commonly referred to as Section 199A. Of all the changes TCJA brought, Section 199A has probably been the most discussed and most thoroughly analyzed.

The deduction applies to individuals who receive income from domestic pass-through entities.

What is a pass-through entity?

Pass-through entity types are legal entities that are taxed at the ownership level, not the entity level. Sole-proprietors, partnerships and S-Corps are all pass-through entities. C-Corporations are not a pass-through entities, as they are taxed at the entity level. In other words, owners of pass-through entities are taxed for the income of the business on their individual Form 1040. Filing Form 1065 (Partnerships) or Form 1120-S (S-Corporations) does not result in tax due for the entity itself. C-Corporations pay tax on their earnings and file Form 1120, and the owners also pay tax when they receive dividends from the business. In that regard, the earnings of C-Corporations are taxed twice.

This includes trusts and estates as well. (However, further discussion is beyond the scope of this blog post).

How much is the QBI deduction?

The QBI deduction can be up to a 20% deduction. Stated differently, your business’ Qualified Business Income, multiplied by 20%. Enormous. Multiply that amount by your marginal tax rate, and that’s the amount you may be able to save in taxes.

However, there are other factors to consider. There are several factors that come into play when taxable income hits certain levels. For 2019, those levels are $160,700 for if filing single, and $321,400 for married filing jointly. If your taxable income is below that amount, no sweat. However, if your taxable income is above the threshold:

1) your QBI deduction may be limited to a percentage of W-2 wages paid by the business, and

2) SSTB rules come into play.

What is Qualified Business Income (QBI)?

Qualified Business Income (QBI) is the net income (revenue less expenses) from your business, with a few exceptions. Guaranteed payments from partnerships, reasonable compensation paid to an S-Corp shareholder, investment income, and some dividends are all excluded from calculating QBI. To be included in QBI, the amounts must be domestically connected.

What is an SSTB?

An SSTB is a Specified Service Trade or Business. If the QBI is from a SSTB, then the amount of the deduction is limited above the thresholds outlined above. SSTBs are businesses in the fields of:

- Health

- Law

- Accounting

- Actuarial Science

- Performing Arts

- Consulting

- Athletics

- Financial Services

- Brokerage Services

- Any trade or business where the principal asset of that trade or business is the reputation or skill of one or more of its employees

- Any trade or business that involves the performance of services that consist of investing and investment management, trading, or dealing in securities

Is a marketing agency an SSTB?

The short answer is “no.” Phew!

However, there is a long answer. You will notice that neither “Marketing” nor “Advertising” are listed above. However, there are two categories which appear to be “catch-alls”:

1) Consulting and

2) “Reputation or Skill”.

Let’s explore both of those.

Are marketing agencies classified as consultants for the purpose of the QBI deduction?

Per the IRS’s final regulations, page 221:

the performance of services in the field of consulting means the provision of professional advice and counsel to clients to assist the client in achieving goals and solving problems.

Sounds like marketing, right? To be honest, I find the final regulations issued by the IRS to be a bit difficult to follow. In my opinion, a recent Journal of Accountancy article does a much better job of concisely laying out how this applies to marketing agencies:

The determination of whether clients are considered to be involved with consulting services is a facts-and-circumstances, case-by-case scenario. When making this determination, a CPA should look for instances where the client is providing recommendations and advice without any type of corresponding goods or services, especially if the client is providing a formal written recommendation report.

This is the difference between a marketing agency and a marketing consultant. Marketing agencies or firms that provide advice and act on that advice, are not SSTBs. Marketing consultants, however, generally are. An example: A marketing agency will say, “You should run $100 in Facebook ads with this picture and this text” and then go and run the ads. A marketing consultant will say, “You should run $100 in Facebook ads” and then somebody outside the consultancy will execute. Advice plus doing is not a SSTB. Advice without the doing is a SSTB.

How does the “reputation or skill” category apply to marketers?

Thankfully, the IRS narrowed this definition with the final regulations. Here, the definition is as follows from pages 227-228:

(A) A trade or business in which a person receives fees, compensation, or other income for endorsing products or services,

(B) A trade or business in which a person licenses or receives fees, compensation, or other income for the use of an individual’s image, likeness, name, signature, voice, trademark, or any other symbols associated with the individual’s identity,

(C) Receiving fees, compensation, or other income for appearing at an event or on radio, television, or another media format.

(D) For purposes of paragraph (b)(2)(xiv)(A) through (C) of this section, the term fees, compensation, or other income includes the receipt of a partnership interest and the corresponding distributive share of income, deduction, gain, or loss from the partnership, or the receipt of stock of an S corporation and the corresponding income, deduction, gain, or loss from the S corporation stock.

In other words, are you endorsing marketing products or services? Are you acting as an influencer? If you’re not, then this classification doesn’t apply.

How is the QBI deduction calculated?

The actual calculation is fairly nuanced. For 2019 and forward, the IRS recently announced the use of Forms 8995 (simplified) or 8995-A (complex) to calculate the deduction.

For marketers, at a high-level, the QBI deduction for a qualified trade or business is the lesser of:

- 20% of qualified business income,

- the greater of: (a) 50 percent of the business’s W-2 wages (applies to most businesses), or (b) an amount based on a more complex formula involving the business’s W-2 wages and its depreciable property (see “Alternative limitation for rental real estate activities”, below).

Confused yet?

You should be.

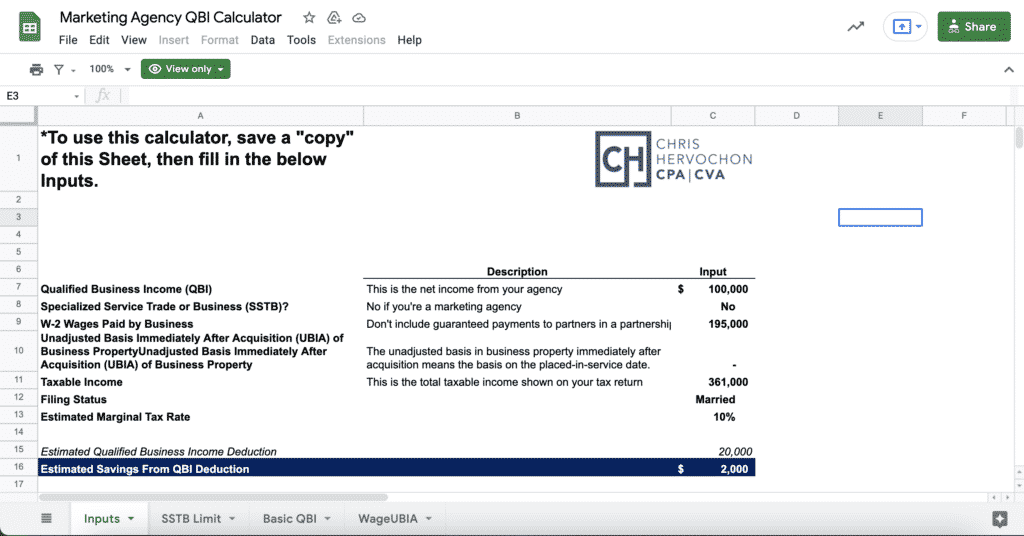

Want to estimate your tax savings due to 199A?

Check out this calculator I created, specifically for marketing agencies, to estimate your deduction. The calculator is also at the bottom of this page. Otherwise, give it a try the old-fashioned way by filling out Form 8995-A (currently in draft) to see what you come up with.

QBI if your marketing agency is an S-Corp

Most of my marketing agency clients are S-Corps or LLCs taxed as S-Corps. The S-Corp structure is fairly popular among marketers, for obvious reasons. In the context of QBI, the biggest issue is reasonable compensation. If you’re an S-Corp owner, you must pay yourself reasonable compensation. However, the portion of your wages from your S-Corp that are reasonable compensation do not factor in for 199A purposes. There’s a balancing act that needs to happen here, depending on your taxable income level.

For a more detailed analysis, the Bradford Institute has a really good article about reasonable compensation after 199A.

How can marketers maximize their QBI?

As outlined above, marketing agencies generally do not fall into the SSTB bucket, so that’s good. Marketing agencies generally aren’t heavy on fixed assets, either. For the most part, marketing agencies have computers, software, office furniture and perhaps a building. Further, many agencies are now remote, working from home. Therefore, the limitations around qualified property are less of a concern, but still a consideration.

Further, the biggest planning opportunity for marketers is likely to be around the compensation you receive from your business. As I mentioned before, and as is outlined in the Bradford Institute article, this is a balancing act. If you need help in determining your optimal compensation, reach out to a tax professional.

But, I don’t itemize my deductions any longer due to the new tax law

It doesn’t matter whether or not you itemize your deductions. QBI is not dependent on whether or not you itemize. If you meet the conditions outlined above, you can take the QBI deduction regardless of whether or not you itemize.

Tying this all together

The final regulations issued by the IRS in January are 211 pages long, so every nuance is not covered here. Instead, this was meant to be a high-level overview, specific to marketers.

Back to the original question: Can marketers take advantage of the QBI deduction? Absolutely.

In fact, marketing agency owners are in a great position to do so since they are not SSTBs. However, agency owners which are S-Corp shareholders should work with a CPA to maximize their 199A tax savings. In particular, as it pertains to the required reasonable compensation.

If Section 199A excites you, and you want to learn more, check out the IRS’s FAQ page related to the deduction.

Finally, if you’re an agency owner, this is potentially a huge tax savings for you. Make sure you’re taking full advantage.

Are you a marketing agency or a marketing professional?

Click here to access the QBI Calculator today.